Partially Updated : 21 January 2022

Contents

- Overview

- A Simple Investment Plan

- Why Fundsmith Equity Class I Accumulation fund?

- Fundsmith Equity vs other Funds and Trusts

- How to beat Warren Buffet

- Which is best : Hargreaves Lansdown or AJ Bell?

- Beware Market Cycles and How To Time Fund Investments

- How to invest a lump sum - all at once or gradually?

- Recommended Books

- Links

- Important Caveat

- £100 Reward

- Important Conclusion

- You need money to invest to make money.

- It only works in a (mostly) rising market.

- Open a stocks and shares ISA with your preferred platform (eg. Hargreaves Lansdown etc.).

- Buy 20K of Fundsmith Equity Class I Accumulation fund

- Repeat each UK tax year

- If you've over 20K per year to invest open a fund and share account also and buy more Fundsmith Equity Class I Accumulation

- Fundsmith Equity has grown 5X more than the FTSE100.

- Fundsmith Equity has grown 2.2X more than the MSCI world index ( MSCI World ).

- Fundsmith Equity has grown 1.5X more than the S&P500.

- Fundsmith Equity has grown by 18.7% per year, on average, after deducting the fund fee.

- Fundsmith Equity has grown by 1.5% per month, with 71% of months being positive, since November 2010.

- Has Terry Smith just been consistently very lucky for the last 10 years and 7 months?

- Are there reasons to think the excellent relative performance of Fundsmith Equity will continue?

- How well is Fundsmith Equity placed to handle the inevitable crash / bear market?

- Google "morningstar fundsmith equity I acc chart"

- If asked choose "private investor".

- On the chart click "advanced Graph"

- On the time scale click "10Y" (or "Max").

- Click on the "x" of unwanted funds to remove them from the comparison.

- Click the "Compare" button.

- Enter your desired comparison fund / trust in the compare box.

- To save your chart Click on "Chart Settings" button, then "print/Export".

- ROCE : Return on Capital Employed : measures how efficiently a company is using its capital to generate profits (higher is better).

- Operating margin : measures revenue after costs (higher is better).

- Interest Cover : measures how well a company can pay the interest on its debts - and thus how risky it is to lend to (higher is better).

-

The DIY Investor: How to take control of your investments and plan for a financially secure future, Andy Bell

Essential reading. An excellent concise and general book. -

How To Own The World, Andrew Craig

Essential reading. Quite long, very readable, excellent background to economics and how poor your kids' retirement will likely be if they don't invest. Covers why financial advisors are mostly useless and how you can easily do much better yourself, especially with modern investment platforms and low fees. -

Stop Saving Start Investing: Ten Simple Rules for Effectively Investing in Funds, Jonathan Hobbs

A very concise book just about funds -

Investing for Growth: How to make money by only buying the best companies in the world - An anthology of investment writing, 2010-20, Terry Smith

Much of the info within is available on the Fundsmith website (eg. the 10 annual reports to shareholders), but useful reading for a deeper understanding of his approach and why it has a good chance to boost your wealth in a relatively reliable and stress free way. - Warren Buffet's advice

- Sharpe Ratio and other Investment Risk measures

- markets.ft.com Fundsmith Equity chart

- Growth over 10 years

- Growth consistency over 10 years

- Financially robust constituent companies as measured by ROCE, Operating Margin, Interest Cover and year of incorporation.

- A cautious long term approach to investing as explained in the Fundsmith Owner's Manual.

Overview Top

This is the lazy person's simple guide to wealth, featuring the kind of specific details you won't find in any finance book (that I've ever seen). It's for my own use only - read at your own risk.

There are just 2 catches :

This webpage is UK orientated but presumably you can also invest in Fundsmith Equity from any country via your preferred investment platform.

Before rushing to the bank please be sure to read the Important Caveat and the Important Conclusion .

A Simple Investment Plan Top

Job done!

Why Fundsmith Equity (FE) Class I Accumulation fund? Top

The Fundsmith Equity fund was started on 1 November 2010 and is run by Terry Smith.

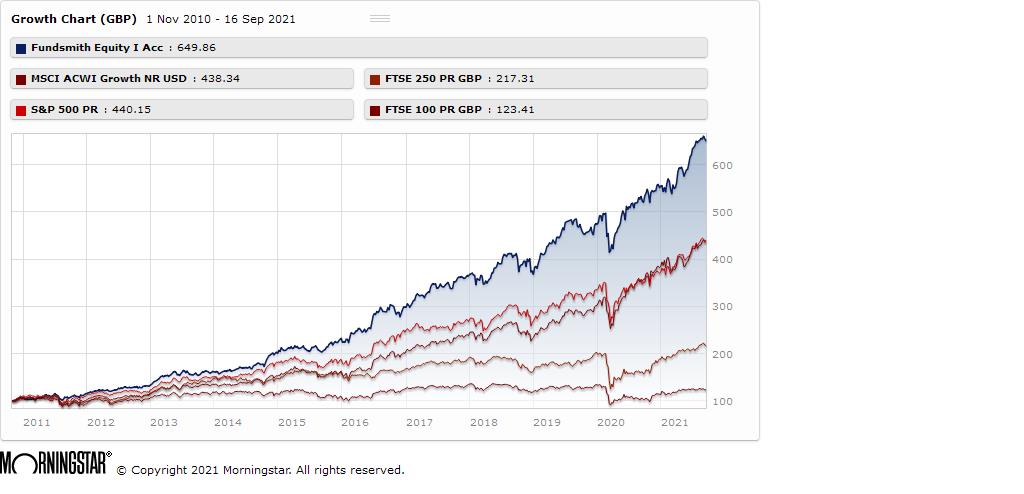

Fundsmith Equity vs MSCI, S&P 500, FTSE 250 and FTSE 100

(see next section for how to create the above chart).

So if you began in November 2010 with £100 in Fundsmith Equity you would now have £649.

If you began in November 2010 with £100 in the FTSE 250 you would now have £217.

If you began in November 2010 with £100 in the FTSE 100 you would now have £123.

etc.

Note also how slow the FTSE indices are to recover from the spring 2020 Covid crash and that the FTSE 100 approximates a horizontal line.

Interestingly if you add the (tech-heavy) NASDAQ to the chart it's above Fundsmith - worth investigating?

Since it began in November 2010 (10 years and 7 months ago) Fundsmith Equity has grown by 623%.

Pretty good! But you might ask :

The short answers (I think) are : no, yes and considerably better than most funds.

To fully understand why I recommend reading Terry Smith's book "Investing for Growth - how to make money by only buying the best companies in the world"

In a nutshell Terry Smith's investment philosophy is "Buy good companies, don't overpay, do nothing". He avoids over trading in search of short term gains and never buys weak companies in the hope their share practice might improve. The 20 to 30 companies held by Fundsmith Equity are financially significantly far more solid than the average S&P500 company and have an average year of incorporation of 1925.

For more details on the financial strength of Fundsmith Equity companies see "How to beat Warren Buffet" below.

The result of this approach is that Fundsmith Equity is signficantly lower risk than most funds or indices and better able to weather market downturns and pandemics. In a given year you might get a higher return from a risky Bailie Gifford fund (perhaps temporarilly benefiting from the Tesla bubble for example) but personally I wouldn't wish to invest in such funds after recent massive gains after a longbull market.

My conclusion is that Fundsmith Equity is an excellent choice for considerable gains with relatively low risk and volatility.

Fundsmith Equity and Indices growth by year (from 100) :

| Fund | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 |

|---|---|---|---|---|---|---|---|---|---|

| Fundsmith Equity | 118 | 126 | 102 | 122 | 128 | 116 | 125 | 121 | 115 |

| MSCI World | 110 | 120 | 95 | 110 | 126 | 102 | 110 | 117 | 109 |

| S&P500 | 113 | 124 | 100 | 109 | 131 | 104 | 119 | 122 | 109 |

| FTSE 100 | 86 | 112 | 88 | 108 | 114 | 95 | 98 | 110 | 107 |

To me the above table helps confirm the idea that perhaps the next best "pay in and leave it" investment after Fundsmith Equity would be a low cost S&P500 tracker, maybe with Vanguard, as per : Warren Buffet's advice .

Fundsmith info :

Annual letter to shareholders 2020

Fundsmith Analysis from AJ Bell

Fundsmith annual shareholders meeting 2021 (video)

Fundsmith Equity vs other Funds and Trusts Top

Method used to create and save these charts :

Fundsmith Equity vs Lindsell Train

Lindsell Train is sometimes recommended as an alternative to Fundsmith Equity. From the chart it's clear it matters very much what version of Lindsell Train you choose. Lindsell Train Global Equity shows fairly steady growth but less than Fundsmith. Lindsell Train Ord (Investment Trust) has risen higher than Fundsmith but is all over the place - if you bought it at the peak in early 2019 you would have had months of huge losses and would still be down now - depressing!

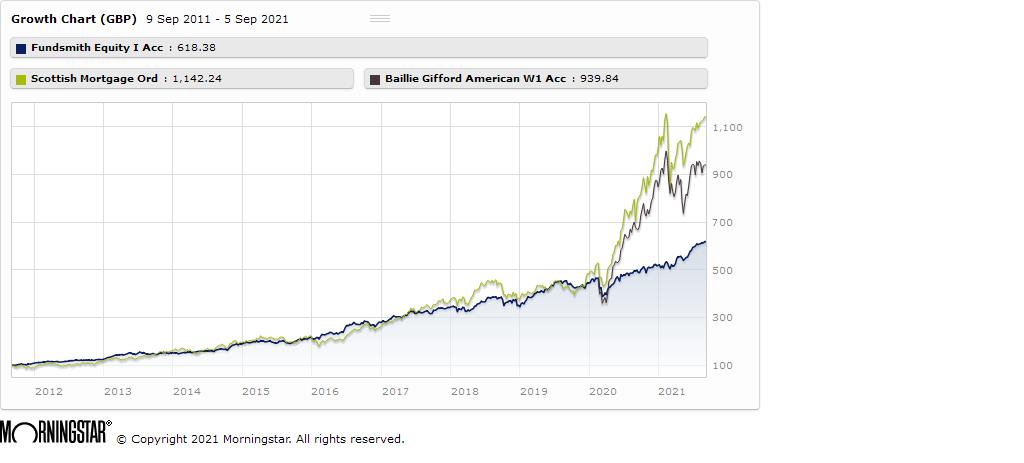

Fundsmith Equity vs Scottish Mortgage vs Baillie Gifford American

With hindsight we see (as of 5 Sep 2021) you'd be better off if you'd bought into Scottish Mortgage or Baillie Gifford American in January 2020 than if you'd bought Fundsmith Equity. But which is the best fund to buy into now? If you'd bought SM or BGA in early 2021 then you'd have immediately lost money and 8 months later you'd still be worse off. Personally I'm very wary of funds with such sudden extreme growth - I expect a sudden and extreme fall may be imminent. Why exactly has Scottish Mortgage more than doubled in value in around 18 months? Is that growth sustainable or a bubble (perhaps a tech stock bubble?).

Note that through it's almost 11 year history there's never been a particularly bad time to buy Fundsmith Equity (although a full recovery from the Spring 2020 COVID crash took 3 or 4 months, as per the market generally).

Perhaps a major reason investors lose money is they can't resist buying whatever has grown the most recently, which often means buying a fund or stock at the wrong time - just before it's sector bubble cools off.

And perhaps another key reason is newbies (like me) pile into the market enthusiastically near the end of a long bull market.

In conclusion Scottish Mortgage and Baillie Gifford American may perhaps be overvalued right now but Fundsmith Equity is a good choice if you fancy a steady growth of 18+% per year with the minimum risk, based on solid companies and avoiding temporary market sector bubbles. Having said that perhaps the entire market is a big overvalued bubble currently! Maybe gold is the thing?

How to beat Warren Buffet Top

Warren Buffet (the "Sage of Omaha") might be the most quoted financial guru ever. You may know that he famously recommended that the cash left to his wife be invested 10% in short-term government bonds and 90% in a very low-cost S&P 500 index fund.

If you'd like to beat Buffet (by some margin) check out the table below which compares the annual return and financial fundermentals (ROCE, Operating Margin and Interest Cover - aggregated for all member companies) of Fundsmith Equity vs S&P500 vs FTSE100, for the year 2020.

Performance and Financial Health for the year 2020 :

| Measure | Fundsmith | S&P 500 | FTSE 100 |

|---|---|---|---|

| Return (growth) | 18.3% | 13% | -11.5% |

| ROCE | 25% | 11% | 10% |

| Operating Margin | 23% | 12% | 9% |

| Interest Cover | 16x | 6x | 6x |

Yes, the FTSE 100 return for 2020 was negative 11.5%.

Explanation of the Measure column above :

So, in 2020, not only does Fundsmith Equity beat the S&P500 return by 5.3% (and the FTSE100 by 29.8%), it does so using companies whose operating fundermentals are far better than the average S&P500 (or FTSE100) company.

This suggests (I think) that the Fundsmith Equity fund is in good shape to weather market downturns, crashes, pandemics etc.

Fundsmith Equity compile the above figures every year and the FE figures are very consistent each year and always far better than the S&P500 and FTSE100.

Apart from consistently high annual returns and robust member companies does Fundsmith Equity have any other advantages over other funds, investment trusts or index trackers?

I think so. The Fundsmith Owner's Manual is worth reading to understand how and why this fund is probably more reliable than any other high performing fund or trust and less vulnerable to market sector bubbles.

Here are a few selected extracts from the Fundsmith Owner's Manual :

We aim to run the best fund there has ever been, and certainly aim to provide the best fund you have ever owned.

.... By best fund, we mean the one with the highest return over a long period of time, adjusted for risk.

You may think it’s odd that by best we don’t necessarily mean the fund with the highest return, certainly not over any short period of time or irrespective of how the returns are achieved. Investment is subject to a lot of fads and cycles. A good example was the Dotcom mania when Technology, Media and Telecommunications stocks rose to valuations which could not be supported by any rational analysis. If you weren’t invested in technology stocks in that period (and we wouldn’t have been) then you would have underperformed the market. We would be happy to have done so, as we would never own a share in a company which we did not think was both good and at worst fairly valued. We would not own something because it is fashionable and might go up.

Because eventually it goes down. Usually by a lot.

There are also funds which deliver high returns but which are running what we would regard as unacceptable risks. They may be following fads, like the Dotcoms, and hoping to sell out and realise the gains before the bubble bursts; or using leverage

or borrowed money to enhance returns, which is OK until things go wrong and the leverage magnifies the losses, or worse.

Most investors make some classic mistakes which prevent them from capturing the best investment performance they could obtain. They buy at the top and sell at the bottom of markets or share price cycles, motivated by greed and fear. It takes considerable emotional discipline to buy when others are fearful and sell when others are greedy. Not that we intend to indulge in market timing, but just doing nothing takes iron discipline when faced with the fears and temptations of the markets.

Which is best : Hargreaves Lansdown or AJ Bell? Top

Hargreaves Lansdown, hands down (as of 27 August 2021).

Admittedly I said "hands down" partly for the rhyme. Of course there are pros and cons and it depends on your priorities and each platform evolves over time so any advantage one has may not last.

I've used HL for several months and they've been very good. HL and AJB offer similar functionality but AJB has an annual charge of 0.25% of your portfolio (under £250K) while HL charges 0.45%. So why would anyone use HL over AJB? AJB have extra buying and selling charges on top of their 0.25%, HL has discounts with many funds that AJB may not have (HL has more customers and is able to negotiate discounts with some funds), HL has many more funds to choose from than AJB has.

Also the HL app is vastly better than the AJB app and I trust HL to increment my investments in line with the market but not AJB.

By the way, while on this topic I've read that if you build up a large and complex portfolio (or any non-trivial portfolio) on one platform and then decide to move to another it can be a slow, frustrating and nerve wracking process. So if considering more than one platform it may be worth opening a small test account with each of them to see how you get on with the interface. You can read lots of platform comparisons that tell you x, y and z are the pros and cons of platform P. Then you try platform P and find the glaring issue / problem for you is something totally different (read on).

I recently opened an account with AJB and bought a little Fundsmith Equity, thinking I should probably switch to them for the lower annual charge. I found their app to be prehistoric compared with HL - they obviously don't take it very seriously. To log in you have to provide 3 characters from your long password and report your first pet (never mind that you have an iphone with face recognition). And then the app tells you almost nothing useful (today's change - not there!). I'm not at all convinced AJB incremented my holding in line with it's market growth - but it was too hard to use the app to check this properly. So I'm giving up on AJB. They recently said they will improve the login process in a few months. But probably will still provide a very poor app once you log in and perhaps fail to increment your investments! Also the AJB app seemed to have no help or method to contact them to ask why they never seemed to increment my investment, while the same investment grew well with HL.

So are HL perfect? Nope. You can use their recommended funds for some guidance but definitely need to look elsewhere to work out the best investments for you (but this is super easy - the answer is "Fundsmith Equity", every time). Remember HL strongly promoted the dodgy (ultimately catastrophic) Neil Woodford fund, and now what I believe to be the best fund going (Fundsmith Equity) isn't on their recommended list. HL claim Fundsmith Equity is omitted simply because the required data was unavailable for analysis. This claim rings alarm bells. Fundsmith Equity provide masses of data on their website. To me it means either that HL are incompetent fools (unlikely?), or too lazy to do their job properly or that they have personal issues with Terry Smith and are putting these above good customer advice. In any event it reflects badly on HL and the credibility of their advice, in my view. Why are HL the only company in the world who are unable to analyse Fundsmith Equity? Fishy.

Also levels of support from HL suffered a little in recent times I think as they have been super busy as many thousands of new customers have come onboard. I think this is typically a sign the market is close to a major negative correction? Eek!

A lot of the recent growth in home investors may be due to millions of extra folk working from home or furloughed. And perhaps folk (such as myself) becoming aware of how good, easy to use and cheap modern investment platforms such as HL are. Still, it's probably largely the investment mania we always see at the end of a long bull market, just before a huge crash ...

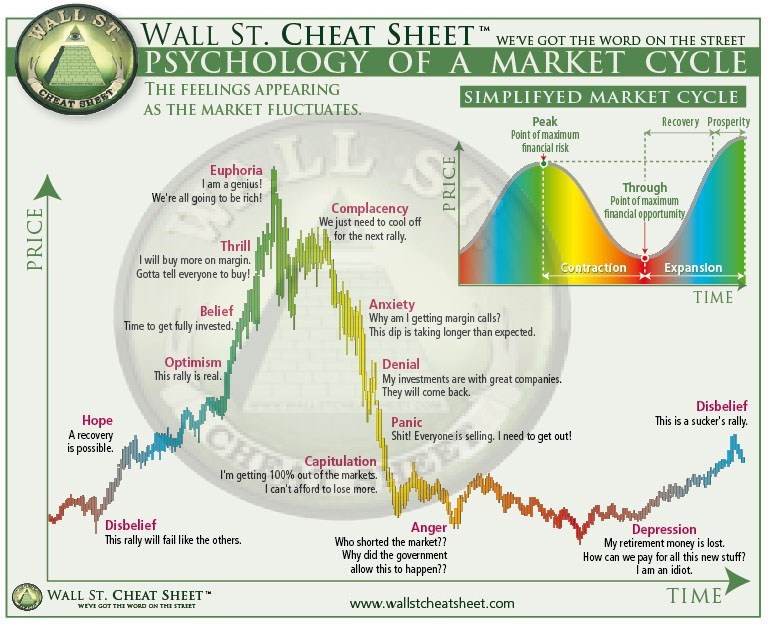

Beware Market Cycles and How To Time Fund Investments Top

Where's the Market right now? Maybe just below Euphoria?

From : are-we-in-a-stock-market-bubble

Interesting FT article : Learning from market bubbles past

A consensus amongst experienced investors seems to be "don't try and time the market" - because nobody can do it successfully (not only do you have to predict events but also predict how the market will react to them and exactly when, by how much and for how long) and also because more money is allegedly lost in preparations for a predicted crash than in the actual crash, and because gains just before a crash are often very large, and because gains when the crash recovers are often really fast (you don't want to miss those by being out of the market).

That's all fine if you're making regular small-ish payments into your funds, but what if you've a huge life changing lump sum to invest? If you'd invested your life savings in 2000 in the S&P500 they would have plummeted and (allowing for inflation) only surpassed their 2000 value after about 16 years!

By late 2007 the markets seemed to be okay again but then another financial crisis struck, shares plummeted and took 6 years to recover.

On this graph choose 30 years, turn off "Show Recessions" and "Log Scale", keep on "Inflation-Adjusted" (don't invest any money without first studying this chart carefully) : S&P500 graph

It's a very scary graph (and bear in mind this is one of the most successfull indices ever - the S&P500). I guess if the market seems over-heated (like now) it's safer to invest a large sum in chunks over time and to try and place each chunk just after you think any significant dip has ended (which you can never tell until the future!).

If ignoring the experts and trying to time an investment into Fundsmith Equity my method would be to view it's chart at FT (see link below), select a suitable time period, hold up my see through ruler to the chart (my advanced analysis of if it's above or below trend!) and also to turn on the Bollinger bands option on the chart and the Exponential Moving Average option. If it's at the Bollinger midline or below and it's below the Exponential Moving Average then perhaps now is a good time to buy more.

markets.ft.com Fundsmith Equity chart

An extra problem, of course, if trying to time the market when buying or selling funds is you don't know their exact price when you place the instruction. I think Fundsmith Equity is priced at noon UK time but your buy / sell order has to be placed before about 8am or the previous afternoon / evening. So making very large fund purchases or sales at a time of high market volatility is risky.

The good news for holders of Fundsmith Equity, in the event of a large market crash is that the financially solid low risk investment philosophy adopted by Terry Smith both in selecting companies and in running the fund means it is likely to outperform the market and to recover well. The most vulnerable assets (my guess is) are those whose valuations depend on Greater Fool Theory (eg. Tesla, Bitcoin, Tulips), those that are highly leveraged, those with low profit margins, and funds lacking liquidity - all of which are avoided by Terry Smith.

We seem to be in a bubble now (Sep 2021). What will it be called? Tech Bubble? Though many of the leading tech companies (Tesla Excepted) appear quite solid with real profits.

How to invest a lump sum - all at once or gradually? Top

I wish I knew! Say you start the year with £24,000 to invest should you invest it all at once in January or invest £2000 every month (dollar cost averaging)? Googling the question suggests investing it all at once is statistically usually slightly better than gradually (which makes sense bearing in mind markets are rising more often than falling, historically), but the difference is quite small.

A fundermental rule of investing seems to be that nobody (experts included) can reliably and consistently time the markets. Another rule is that markets go up more than down. So it follows (statistically) that the longer you have the most money invested the better, especially if you pick wise investments.

My friend Alan has a different view. His first significant investment, under expert guidance, was largely tech orientated and made at the height of the dot.com boom. Very soon his investment plummeted and took about 16 years to return to it's starting point.

If gradual investment is statistically only slightly less rewarding than up front investment then maybe it's a better choice to reduce the risks of making a big investment just before a crash, especially in an overheated market.

This article is interesting on the topic : does-market-timing-work. Alas when you look closely is doesn't really compare lump sum vs gradual. The "lump sum" here means $2000 paid every year for 20 years (which I call gradual with annual frequency). It would have been helpful if they'd done a proper lump sum in the comparison ($20,000 paid at the start of the 20 year period).

Of course your choice must depend very much on your full financial circumstances, age and attitude to risk.

Recommended Books Top

Links Top

Important Caveat Top

I'm quite new to investing (and may be an idiot) so do take this web page with a dose of salt, check the sources and draw your own conclusions.

Although I can't find anything so far as high performing and apparently reliable as Fundsmith I expect it's wise to have a slightly wider portfolio! A low cost S&P500 tracker (as recommended by Warren Buffet) is probably a good idea?

£100 Reward Top

For the first person who can find me a fund or trust (funds preferred) that can exceed Fundsmith Equity on the following criteria :

Good luck! I expect you'll fail but if such a fund exists I'll be delighted to pay you £100 reward and to invest in it myself.

Important Conclusion Top

As of 14 January 2022 : The current S&P500 10-year P/E Ratio is 38.0. This is 90% above the modern-era market average of 19.6, putting the current P/E 2.3 standard deviations above the modern-era average. This suggests that the market is Strongly Overvalued (and a large / very large correction due?).

Source : www.currentmarketvaluation.com/models/price-earnings.php

Conclusion 1 (if (like me) new to investing) : it's worth investing token amounts currently to get familiar with the method, and then waiting for the imminent? big crash before making large investments (no idea how you decide when the bottom is - but the above web site may help?).

Conclusion 2 (if heavily invested already) : it might be worth selling now and holding cash (or gold?), ideally before the crash.